Improper Disclosure of Deferred Down Payments

One of the most common illegal tricks that California car dealerships use to close sales is failing to properly disclose the buyer or lessee’s deferred down payments. This practice is not permitted by California’s Automobile Sales Finance Act (sometimes called the “ASFA”), and can result in the buyer or lessee being able to cancel the deal and get his or her money back.

Because the practice is so widespread, all consumers who are interested in canceling their purchase or lease contracts and getting their money back should determine whether they made a deferred down payment, and if so, whether the dealer disclosed the deferred down payments in manner required by California law.

How Can I Tell If I Made A Deferred Down Payment?

It is very easy to determine whether or not you made a deferred down payment. A deferred down payment is any portion of the down payment that you paid to the dealer on a date after the date on which you signed the contract. For example, if your total down payment is $2,000, and you immediately paid the dealer $1,500 and agree to return two weeks later to pay the remaining $500, then you made a $1,500 cash down payment and a $500 deferred down payment. Similarly, if you gave the dealer a post-dated check, or otherwise agreed that the dealer could not deposit your down payment check until a specific date, then the agreement to hold onto your check amounts to a deferred down payment.

How To Tell If Your Deferred Down Payment Is Properly Disclosed In Your Contract

If you made or agreed to make a deferred down payment with the dealer, you should check to see if the dealer properly disclosed it as a deferred down payment. This page will show you how to do so for both vehicle purchase contracts and automobile lease contracts.

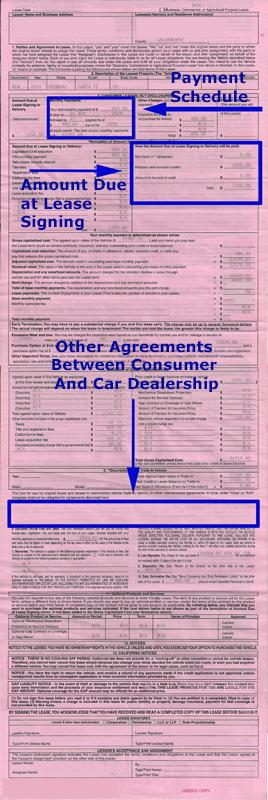

To check whether the deferred down payment is disclosed correctly in a purchase contract, first find the “Total Downpayment” section. This section is included amount many other disclosures in the large box titled “ITEMIZATION OF AMOUNT FINANCED.” It is usually near the bottom of that section. As depicted in the image to the right, if you look at the entire purchase contract, the “Total Downpayment” section is about two-thirds of the way down the page on the left-hand side.

To check whether the deferred down payment is disclosed correctly in a purchase contract, first find the “Total Downpayment” section. This section is included amount many other disclosures in the large box titled “ITEMIZATION OF AMOUNT FINANCED.” It is usually near the bottom of that section. As depicted in the image to the right, if you look at the entire purchase contract, the “Total Downpayment” section is about two-thirds of the way down the page on the left-hand side.

Once you find the Total Downpayment section, check the amounts that are listed beside the “Deferred Downpayment” and “Cash” line items. For example, below is an example of the Total Downpayment section in a vehicle purchase contract. The green arrow points to the “Cash” line, which is where the contract should state the portion of the down payment that you made on or prior to the date on which you signed the contract. The blue arrows point to the Deferred Downpayment line, which should state the amount of the down payment that you agreed to pay on a date that is after the date on which you signed the contract.

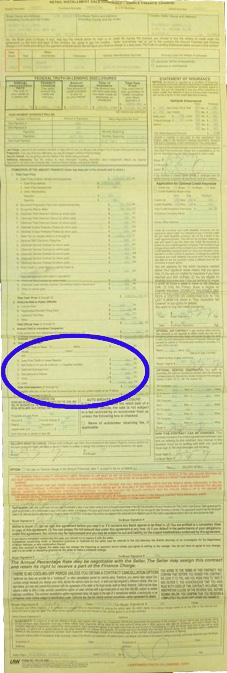

In lease contracts, checking to see if a deferred down payment is properly disclosed can be a little more difficult (but not much) because it could be disclosed in a few places, all of which are highlighted in the image to the right. The blue arrows point to the boxes where your lease should have a “Schedule of Payments” section, a “How Amount Due at Lease Signing Will be Paid” section, and a “Individual Agreements Between Lessor and Lessee” section. These sections could have slightly different names in your lease, but if you leased your vehicle in California they will be in approximately the same locations in your lease contract.

In lease contracts, checking to see if a deferred down payment is properly disclosed can be a little more difficult (but not much) because it could be disclosed in a few places, all of which are highlighted in the image to the right. The blue arrows point to the boxes where your lease should have a “Schedule of Payments” section, a “How Amount Due at Lease Signing Will be Paid” section, and a “Individual Agreements Between Lessor and Lessee” section. These sections could have slightly different names in your lease, but if you leased your vehicle in California they will be in approximately the same locations in your lease contract.

Check all three of the sections. Do anything of them list your deferred down payment and state its due date? If not, check the “How Amount Due at Lease Signing Will be Paid” section. Does the disclosure for the “Amount to be Paid in Cash” include your deferred down payment? If so, then the deferred down payment was likely disclosed in an improper and/or illegal manner.

Contact An Auto Fraud Lawyer If Your Deferred Down Payment Is Not Properly Disclosed In Your Purchase Or Lease Contract

California’s vehicle financing laws are very strict, and if the dealer that sold or leased a vehicle to you failed to properly disclose your deferred down payment then you may have a right to cancel your contract, return the vehicle, and get your money back. Accordingly, if your deferred down payment is not properly disclosed on your contract, contact an experienced auto fraud attorney immediately to discuss your legal rights.

The Vachon Law Firm offers free consultation in all auto fraud, lemon law, and repossession cases. So if you want to find out more about your legal rights, call the Vachon Law Firm today at 1-855-4-LEMON-LAW (1-855-453-6665). We will review your documents, confirm whether or not your deferred down payment was properly disclosed, and explain your legal options for pursuing a refund. You can also contact us via email. Contact us today!

The Vachon Law Firm typically takes deferred down payment cases on a contingency fee basis.

Can I Really Get a Refund Because the Dealer Did Not List a Deferred Down Payment on My Contract?

Generally, yes. Failing to disclose a deferred down payment clearly violates two provisions of the ASFA. First, section 2981.9 in the ASFA requires that all agreements between a buyer and a seller be contained in a “single document” (the “Single Document Rule”). Failing to disclose a deferred down payment violates the Single Document Rule because neither the existence, amount, nor due date of the deferred payment is contained in the purchase contract. Additionally, section 2982(a)(6)(D) of the ASFA expressly requires that car dealers itemize the amount of any deferred down payments. Thus, a failure to disclose a deferred down payment violates this provision as well.

The ASFA also makes clear that a violation of its disclosure requirements results in the buyer being able to rescind the contract and receive a refund. Specifically, section 2983(a) of the ASFA states that a violation of its disclosure obligations renders the contract unenforceable, and section 2983.1(d) states that when a contract is unenforceable the consumer can return the vehicle and obtain a refund (so long as he or she elects to do so promptly).

Because the ASFA is such a powerful statute, and because deferred down payment violations are so common, the ASFA is the “secret weapon” of many lemon law and consumer fraud attorneys, because it allows consumers to obtain refunds in so many cases.

Contact us today to find out if you are entitled to a refund under the ASFA!